Private Credit Sees $15.6 Billion in Redemptions in Q2

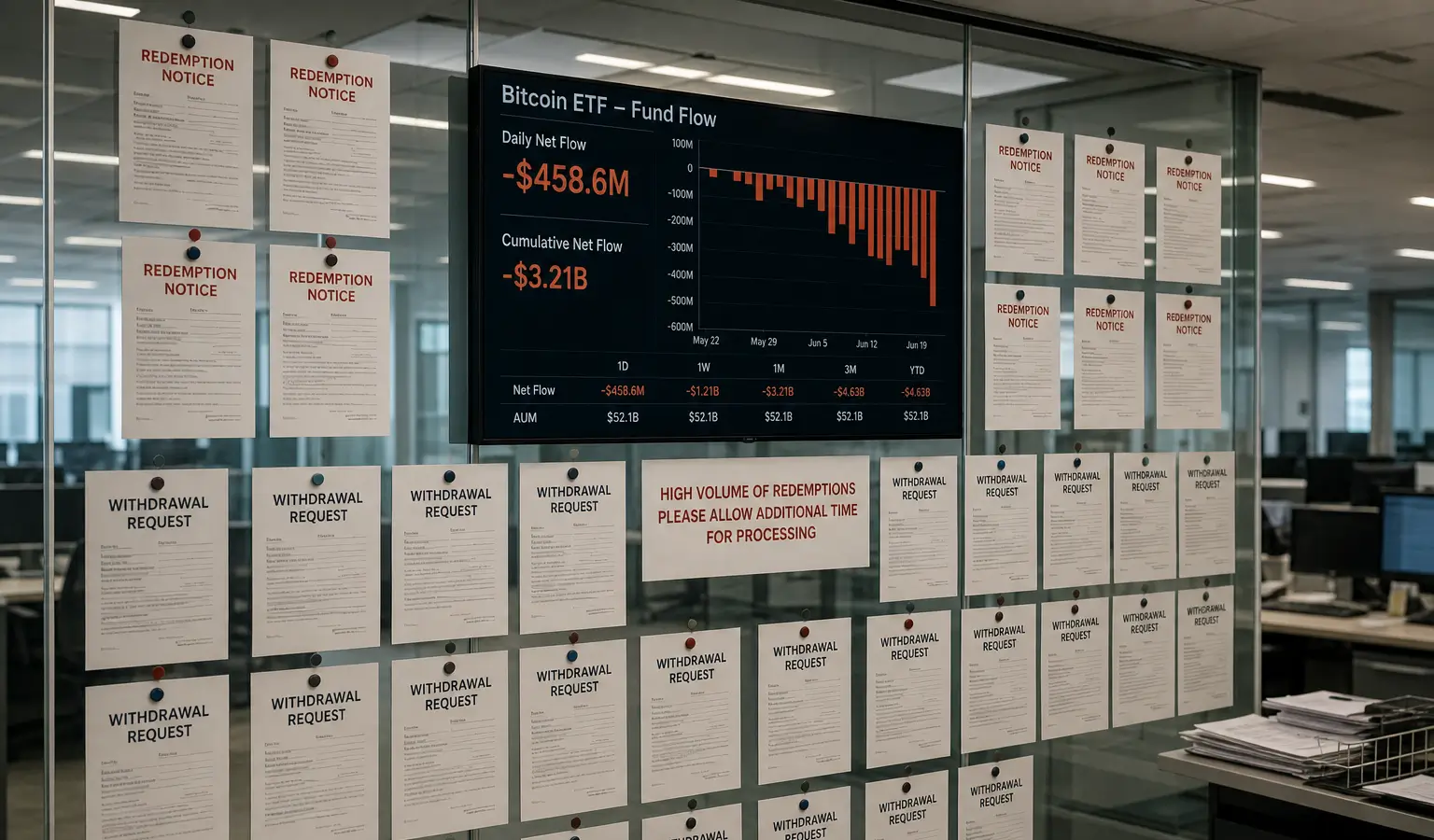

U.S.-listed spot Bitcoin ETFs saw nearly $5 billion in outflows, while private credit was hit even harder with $15.6 billion in redemptions. The numbers point to broader liquidity pressure and weaker risk appetite.

Key Takeaways

- U.S.-listed spot Bitcoin ETFs saw nearly $5 billion in outflows in Q2, while Bitcoin fell about 14% and dropped below $60,000.

- Private credit saw $15.6 billion in redemptions in Q2; many requests were only partly met because of the usual 5% quarterly cap.

- The mix of ETF outflows and private credit stress points to broader liquidity pressure and a more cautious risk appetite in the market.

The Q2 data highlights two markets that both depend heavily on liquidity, but in very different ways. U.S.-listed spot Bitcoin ETFs recorded nearly $5 billion (€4.4 billion) in outflows, while private credit faced an even larger $15.6 billion (€13.6 billion) in redemptions. For crypto investors, the bigger takeaway is that Bitcoin’s weakness fits into a wider picture of softer risk appetite and shifting capital flows.

Bitcoin ETFs Feel the Outflows

SoSoValue data shows that investors pulled about $4 billion (€3.5 billion) from U.S.-listed spot Bitcoin ETFs in Q2. BlackRock's IBIT was among the biggest contributors to June outflows. Over the same period, Bitcoin dropped about 14% and fell below $60,000 (€52,500), extending its losing streak to a third straight quarter.

Market watchers pointed to several possible reasons for the pullback. Some money appears to have rotated into the AI trade and other hot themes, while SpaceX's Nasdaq listing on June 12 also attracted institutional capital, according to analysts. Others, including Strive CEO Jack Mallers, argue the move reflects tightening macro liquidity.

Private Credit Gets Hit Even Harder

The pressure was even more pronounced in private credit. Fitch reported that investors asked to redeem $15.6 billion (€13.6 billion) in Q2 across the $2 trillion (€1.7 trillion) market, but only part of that demand was satisfied. At 10 of the 16 business development companies, or BDCs, redemption requests came in above the standard 5% quarterly cap, leaving many investors with only partial payouts and a wait for future quarters.

Average redemptions climbed to 10.3% of shares, up from 9.7% in Q1. At Blue Owl's OTIC, the range ran from 1.3% to 38.1%. New inflows also dropped by about 56% on average, which left most funds with net outflows of roughly 3% of the previous quarter's net asset value. Fitch expects redemption pressure to remain elevated in the months ahead.

Private credit has expanded quickly over the past 15 years, growing from $158 billion (€138 billion) in 2010 to nearly $2 trillion (€1.7 trillion) by mid-2024. That growth has made the mismatch between investor liquidity expectations and the illiquid nature of the underlying loans more obvious, pushing funds to rely on caps and other limits more often.

Why This Also Matters for Crypto

For European crypto readers, the comparison matters because Bitcoin often reacts early to changes in liquidity and financing conditions. If ETF investors and private credit investors are both becoming more cautious at the same time, that can signal a broader risk-off tone in the market, even if it does not point to a clear price move right away.

The combination of ETF outflows and private credit redemptions also shows that liquidity stress is not limited to crypto. Other investment products are dealing with the same pressure, which makes this a useful moment to watch the connection between crypto, macro trends, and institutional capital flows.